Featured Posts

Financial Services

ATR Op-Ed in American Banker: “The Fed’s manipulation of debit card interchange fees must stop”

On April 25, 2024, American Banker’s commentary page, BankThink, published an op-ed written by ATR’s director of financial policy, Bryan Bashur. The piece…

Spending & Regulatory Reform, Tax Reform

Worst of Both Worlds: U.S. Economic Growth Slows as Inflation Rates Rise

Today, the Commerce Department released a snapshot of its growth report for the first quarter. The country’s gross domestic product (GDP) grew by just…

Tax Reform

No Tax Cut for Kansans, says Governor Kelly after vetoing bipartisan package

Kansas Governor Laura Kelly (D) callously vetoed a bipartisan tax relief package on Wednesday that included income, property, and business tax cuts totaling just $460…

Filtered Posts

Tax Reform

Biden: Tax cuts “are going to stay expired and dead forever if I’m re-elected.”

Joe Biden and Kamala Harris Will Raise Your Taxes

Tax Reform

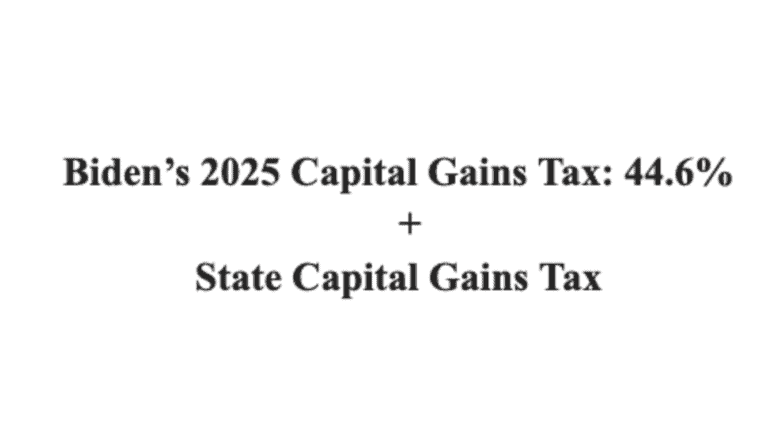

Biden Calls for 44.6% Capital Gains Tax Rate, Highest Capital Gains Tax Since Its Creation in 1922

Tax Reform

Biden’s $400k Tax Pledge Now Only Worth $337k

Spending & Regulatory Reform

Biden Budget Deploys 50,000-Person Green New Deal Youth Patrol

Tax Reform

SOTU: Biden Will Lie About GOP Tax Cuts, Again

IRS Watch, Tax Reform

Norquist Warns of the Privacy Risk of IRS “Bring Your Own Device” Program

IRS Watch, Tax Reform

Congresswoman Carol Miller Calls Out IRS Chief for Illegal Actions on 1099-K

IRS Watch, Tax Reform

IRS Chief Won’t Directly State the Number of Guns in IRS Possession

IRS Watch, Tax Reform