On this day one hundred fifty four years ago Congress and Abraham Lincoln imposed the first ever federal income tax. He saw a growing need for new funds both to back the Union’s Civil War effort and to combat the federal deficit that resulted from the financial panic in 1857—the first world-wide economic crisis.

On August 5, 1861, Lincoln signed the Revenue Act, which placed a 3 percent flat tax on annual incomes over $800. According to the Bureau of Labor Statistics, that would be equivalent to $20,645.04 in 2014 dollars. The broadly worded legislation defined income as profits “derived from any kind of property, or from any professional trade, employment, or vocation carried on in the United States or elsewhere or from any source whatever.”

However, just one year later President Lincoln repealed the flat tax provision and replaced it with a progressive scale that placed a 3 percent tax on incomes between $600 and $10,000 and a 5 percent tax on all incomes higher than $10,000. In 1864, the legislation was amended again to add a third bracket to the graduated scale with the top earners’ incomes subject to a 10 percent tax. Over a decade after the war ended and the Reconstruction was nearly complete, the tax was repealed and found to be unconstitutional.

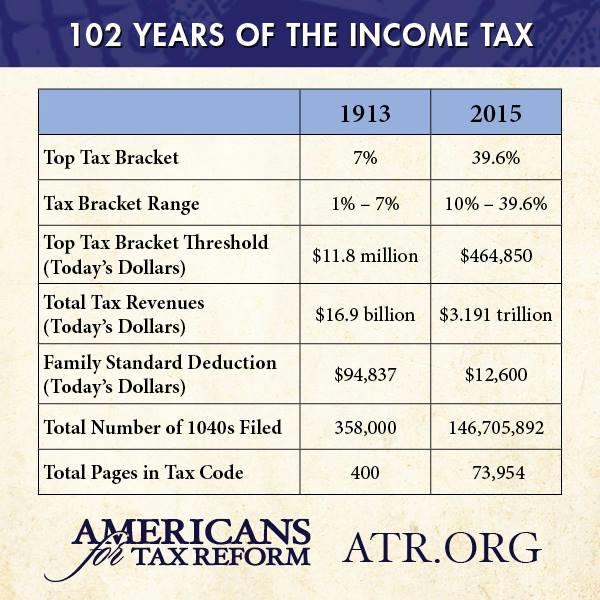

Though the federal income tax didn’t come back to stay until 1913, Lincoln’s first federal income tax laid the groundwork for taxing incomes in our nation’s future. The type of gradualism that was used to increase the federal tax burden in the 1860s is not unfamiliar to modern taxpayers. Throughout its 102-year history, the federal government has taken a mile for each inch taxpayers have given when it comes to the income tax. As a result we now have a needlessly complex tax code that is tens of thousands of pages long and dips deep into the pockets of every American.