Featured Posts

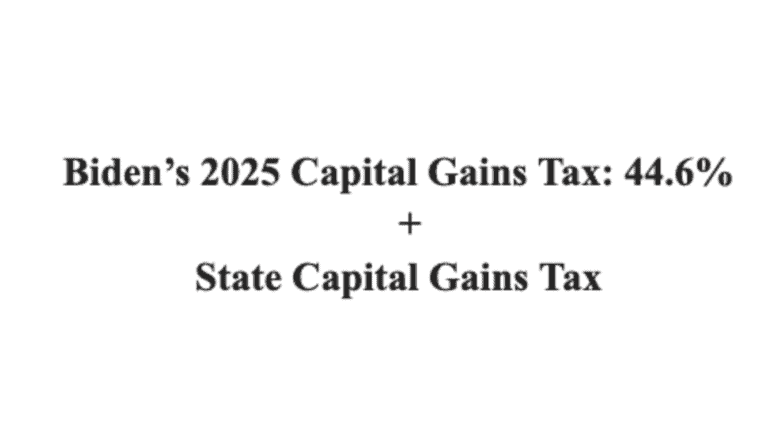

Biden Calls for 44.6% Capital Gains Tax Rate, Highest Capital Gains Tax Since Its Creation in 1922

And don’t forget to add the state capital gains tax: the Biden combined federal-state rate would exceed 50% in many states President Biden has…

Trade

ATR Applauds House Oversight For Investigating FTC-DOJ Strike Force

The House Committee on Oversight and Accountability is launching a probe into the rampant politicization of the Federal Trade Commission (FTC) by Chair Lina Khan…

Taxpayer Protection Pledge

ATR Commends Pennsylvania Pledge Signers Ahead of April 23 Primary

As Pennsylvania Primary voters head to the voting booth, they deserve to know where their candidates stand on crucial issues such as taxes and spending.

Filtered Posts

ATR Releases List of 2015 State Pledge Signers Ahead of Virginia General Election

ATR Releases List of 2015 State Pledge Signers Ahead of New Jersey General Election

The Grover Norquist Show: Corporate Welfare in the Ex-Im Bank & the Federal Sugar Program

Jess Fields Signs Taxpayer Protection Pledge

The Grover Norquist Show: John Kasich’s Tax Plan

New Leadership Must Remain Diligent, Keep Spending Capped

Why Vapers Should Care About the Remote Transactions Parity Act

Hypocritical “Save Lives” Coalition Proposes Tax On Life-Saving Tobacco Alternative

The Grover Norquist Show: The Jeb Bush Tax Reform Plan