Commentary

Tax Reform

Property Taxes Fuel the Local Spending Fire

Income tax rate reduction and elimination has been a top policy trend for more than a decade, but in proposals to reduce or limit…

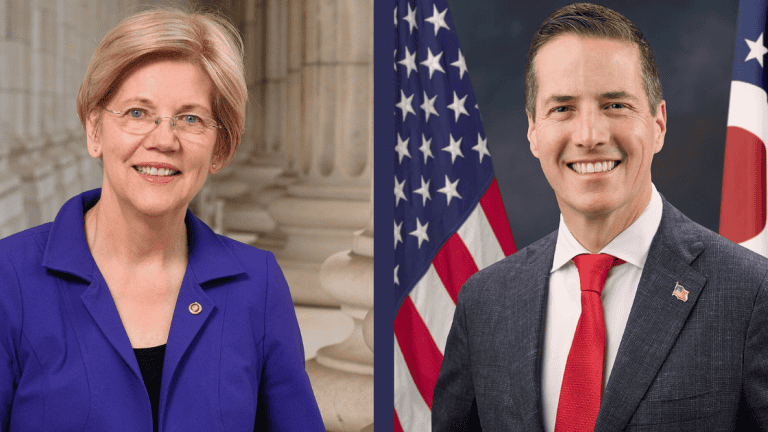

No Conservative Support for Bernie Moreno’s Giant Tax Increase

One month after its unveiling with Elizabeth Warren, no elected or unelected conservative has endorsed Bernie Moreno’s $3 trillion tax increase…

Tech & Telecom, Trade

EU Hits Google with a $1 Billion Fine

In the latest episode of its digital tax craze, the EU forces Google to pay €890 million ($1 billion) under the Digital Markets…

Tax Reform

ATR Backs Trump’s Nomination of Francis Brooke for Deputy Treasury Secretary

Tax Reform

Study: Global Wealth Tax Would Kill 20 Million Jobs and Shrink the Economy

Tax Reform

Left-Wing Advocacy Groups Push Counterproductive $65M Tobacco & Nicotine Tax Hike in Nevada

About Us

Has Your Elected Official Signed the Pledge?

No one in modern times has fought harder to shrink the state than the founder of the group Americans for Tax Reform.

One of the most influential figures in the history of the U.S. tax code and the U.S. budget, a consistent and provocative voice for less of each.

Since creating Americans for Tax Reform at Ronald Reagan’s behest back in 1985, Norquist has been responsible more than anyone else for rewriting the dogma of the Republican Party.

There's been no organization in our country who's kept the issue of high taxes and IRS abuse more in the public eye than ATR.

The high priest of Republican tax-cutting

The Sustainable Budget Project

The Sustainable Budget Project monitors state government spending and tracks which states have or have not enacted sustainable budgets.

Featured Links

About Grover

“Hands down the most powerful tax advocate in Washington.” – The Hill

Coalition Meetings

"The Grand Central Station of the conservative movement." – John Fund

Featured Letters

Spending & Regulatory Reform, Tax Reform

ATR Opposes New Dem Effort to Raise Taxes, the PROMISE Act

Financial Services

ATR Submits Comment Letter on Revised Basel Endgame Proposal

Financial Services

ATR Sends Letter to Governor Jared Polis Urging Him to Veto Senate Bill 26-134

Policy Areas

-

Tax Reform

Tax Reform

-

Spending & Regulatory Reform

Spending & Regulatory Reform

-

Healthcare

Healthcare

-

Tech & Telecom

Tech & Telecom

-

Energy

Energy

-

Labor

Labor

-

Property Rights

Property Rights

-

Financial Services

Financial Services