Featured Posts

Senator Crapo Calls Out IRS Chief for Misleading Congress About “Direct File”

Sen. Mike Crapo (R-Idaho), ranking member of the Senate Finance Committee, questioned IRS commissioner Daniel Werfel yesterday about Werfel’s dishonesty to Congress regarding the IRS…

Financial Services

ATR Supports Fight Against SEC’s Climate Rule

On March 21, 2022, the Securities and Exchange Commission (SEC) introduced a proposed rulemaking that required publicly traded companies to disclose information…

Financial Services

ATR Supports Fight Against CFPB’s Credit Card Late Fee Rule

Without any direction from Congress, the Consumer Financial Protection Bureau (CFPB) finalized a rule that (1) changes the safe harbor dollar amount for late fees…

Filtered Posts

BREAKING: The Kansas Legislature Has Lost Its Mind

ATR Releases List of 2015 State Pledge Signers Following Primary Elections in New Jersey

Comprehensive List of Martin O’Malley Tax Hikes

Michigan Tax Hike Measure Goes Down in Flames, 80-20

Michigan Voters Faced With $2 Billion Tax Hike on May 5 Ballot

Ohio State House Republicans Push A Sound Tax Reform Agenda

Americans for Tax Reform Urges Gov. Hogan to Veto the Maryland Travel Tax Bill

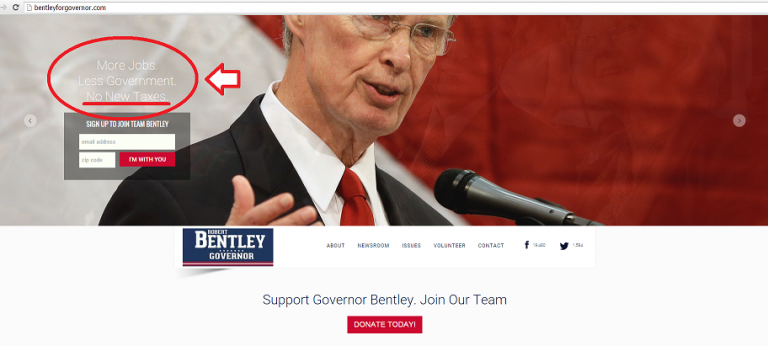

Alabama Governor Insinuates He’ll Release Dangerous Prisoners Unless Lawmakers Raise Taxes

Robert Bentley Breaks His Pledge, Runs From the Truth